The debt snowball method is defined as a debt repayment strategy where you pay off your smallest balances first, then roll each freed-up payment into the next debt on your list. Personal finance frameworks categorize it as a 6-step behavioral strategy built on psychological momentum rather than interest rate math. The method works because each paid-off account delivers a real win that keeps you motivated. That motivation is the engine. Without it, most debt payoff plans stall within months. The snowball approach trades a small amount of mathematical efficiency for a much larger gain in follow-through.

What do you need before starting the debt snowball method?

Preparation determines whether your plan survives contact with real life. Skipping this step is the most common reason people quit within the first 90 days.

Gather every debt you owe. Write down each balance, minimum payment, and lender. Do not sort by interest rate yet. The snowball method intentionally ignores interest rates at this stage. You need the full picture before you can build a realistic plan.

Commit to minimum payments on every account. Missing minimums triggers late fees and credit score damage. Those costs erase any progress you make on your target debt. Minimum payments on all accounts except your smallest one are non-negotiable from day one.

Review your monthly budget for extra cash. Even $50 extra per month accelerates your payoff timeline. Sustainable budgeting is the foundation of the entire plan. Overextending your repayment ability leads to failure and higher total costs.

Here is what to have ready before you begin:

- A complete list of all debts sorted from smallest to largest balance

- Confirmed minimum payment amounts for each account

- A monthly budget that identifies at least one area to cut spending

- A spreadsheet, budgeting app, or free online calculator to track progress

- A written commitment to stop adding new debt during the payoff period

Pro Tip: Use a free credit card payoff calculator, such as the tools available at Apexapro, to model exactly how many months each debt will take to eliminate. Seeing a concrete end date makes the plan feel real.

How does the debt snowball method work, step by step?

The process follows a fixed sequence. Changing the order undermines the motivational logic that makes the method effective.

- List all debts from smallest to largest balance. Ignore interest rates completely. A $400 medical bill goes above a $3,000 credit card even if the credit card charges 24% APR.

- Pay the minimum on every debt except the smallest. This keeps all accounts in good standing while you concentrate firepower on one target.

- Send every extra dollar to the smallest debt. If your budget frees up $150 per month, add it entirely to that smallest balance. Split payments dilute the effect.

- Celebrate when the smallest debt reaches zero. This is not optional. The emotional reward is part of the mechanism.

- Roll the full payment amount into the next debt on the list. If you were paying $200 total on the first debt (minimum plus extra), add that entire $200 to the minimum payment on debt number two.

- Repeat until every account is paid off. Each cycle accelerates because your available payment grows with every account you close.

A concrete example of the snowball in action

Imagine you carry three debts: a $500 store card, a $2,200 personal loan, and a $6,800 credit card. Your minimums are $25, $60, and $140 respectively. You find $100 extra per month in your budget.

| Debt | Balance | Minimum | Extra Payment | Monthly Total |

|---|---|---|---|---|

| Store card | $500 | $25 | $100 | $125 |

| Personal loan | $2,200 | $60 | $0 | $60 |

| Credit card | $6,800 | $140 | $0 | $140 |

You eliminate the store card in roughly four months. Then your $125 rolls into the personal loan, giving you $185 per month on that balance. The personal loan falls in about 12 months. Then $185 plus $140 gives you $325 per month on the credit card. The acceleration is real and measurable. Using the snowball approach saves years and thousands in interest compared to paying only minimums, even without adding new money to the plan.

Pro Tip: Call each lender and explicitly request that extra payments be applied to your principal balance immediately. Some lenders default to crediting extra funds as early future payments, which does not reduce your balance as fast.

Common mistakes that derail your debt payoff plan

Knowing the pitfalls in advance keeps you from repeating the errors that send most people back to square one.

- Applying extra payments incorrectly. Lenders sometimes apply extra funds as advance payments on future due dates rather than reducing your principal. Confirm with your lender that every extra dollar hits the principal directly. This single step can shorten your payoff timeline by months.

- Setting goals that are too aggressive. Cutting your budget to the bone feels disciplined but usually fails. Overly ambitious repayment targets cause people to quit prematurely, which increases total cost. Build in a small buffer for unexpected expenses.

- Getting discouraged on large debts. After the quick wins on small balances, a $10,000 debt can feel like a wall. Progress is still happening even when the balance drops slowly. Track the total amount paid, not just the remaining balance.

- Adding new debt during the payoff period. A new credit card purchase restarts the clock on that account. Freeze discretionary credit use until your list is clear.

- Misunderstanding the interest cost. The snowball method costs more in total interest than the avalanche method when interest rates vary significantly. That tradeoff is intentional. Motivation and completion beat a theoretically cheaper plan that gets abandoned.

"Prioritize the debt causing you the most emotional stress, even if it is not the smallest balance. Financial plans that ignore your emotional state rarely survive long enough to work."

This insight reflects a key customization principle: adjusting your payoff order to address emotional burden improves engagement and long-term adherence, even when it deviates from the strict smallest-first rule.

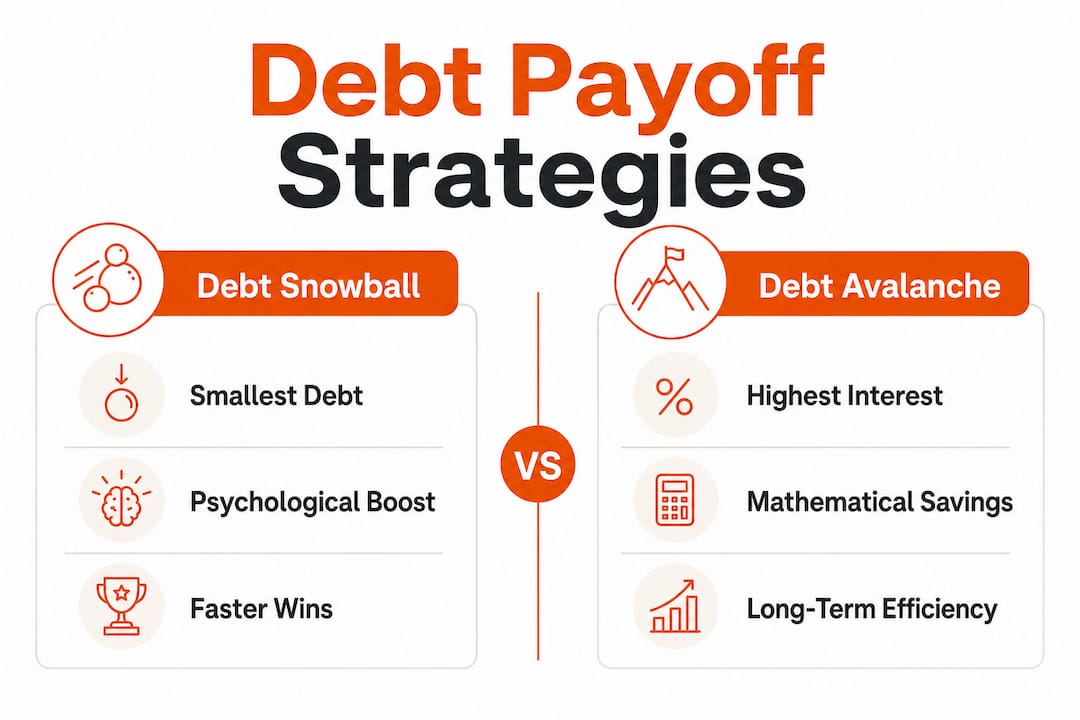

How does the debt snowball compare with other payoff strategies?

The debt snowball vs avalanche debate is fundamentally a question of mindset over math. Both methods work. The right choice depends on what you can sustain.

The debt avalanche method targets your highest interest rate debt first, regardless of balance size. Mathematically, it minimizes total interest paid. The snowball method targets the smallest balance first, regardless of rate. Behaviorally, it maximizes motivation and completion rates.

| Feature | Debt snowball | Debt avalanche |

|---|---|---|

| Payoff order | Smallest balance first | Highest interest rate first |

| Primary benefit | Psychological wins, faster motivation | Lower total interest paid |

| Best for | People who need frequent wins to stay on track | People comfortable with delayed gratification |

| Risk | Higher total interest if rates vary widely | Slower early progress, higher dropout risk |

| Flexibility | Can customize order by emotional burden | Strict mathematical order works best |

The efficiency gap between snowball and avalanche is often small when interest rates across your debts are similar. When rates are close, the snowball's motivational benefits outweigh the marginal interest savings of the avalanche. The choice between the two methods is ultimately a mindset decision: motivation versus efficiency.

Some people combine both approaches. They use the snowball to eliminate two or three small debts quickly, then switch to the avalanche for the remaining high-rate balances. This hybrid works well for people who need early wins but also want to limit long-term interest costs. Neither method is universally superior. The best credit card payoff plan is the one you actually finish.

A third option worth knowing is debt consolidation, where you combine multiple balances into a single loan at a lower rate. Consolidation simplifies payments but does not build the behavioral habits that snowball and avalanche methods reinforce. Many financial counselors recommend pairing consolidation with a structured payoff method for lasting results.

Key Takeaways

The debt snowball method works because psychological momentum drives completion more reliably than mathematical optimization alone.

| Point | Details |

|---|---|

| Start with the smallest balance | List debts from smallest to largest and attack the first one with every extra dollar you have. |

| Roll payments forward | After each payoff, add the full freed-up amount to the next debt's minimum payment to accelerate progress. |

| Confirm principal application | Tell your lender explicitly to apply extra payments to the principal, not future due dates. |

| Keep goals realistic | A budget you can sustain for 12 months beats an aggressive plan you abandon in 60 days. |

| Snowball vs avalanche | Choose the snowball for motivation; choose the avalanche for maximum interest savings when rates differ significantly. |

Why the snowball worked for me when nothing else did

I have worked through debt payoff plans with a lot of people over the years, and the pattern is consistent. The ones who succeed are rarely the ones with the best math. They are the ones who felt something when they paid off that first account.

I used the snowball myself when I had four debts spread across two credit cards, a car loan, and a medical bill. The medical bill was only $340. Paying it off in six weeks felt almost trivial. But that feeling of closing an account, of removing one line from the list, changed how I approached the next debt. The motivation was not theoretical. It was immediate and physical.

The mistake I see most often is people treating the snowball as a pure numbers exercise. They skip the celebration step. They do not tell anyone they paid something off. They move straight to the next debt without acknowledging the win. That kills the momentum the method is designed to build.

My honest advice: customize the order if you need to. If a particular debt is causing you serious stress, pay it off early even if it is not the smallest. Adjusting for emotional burden is not cheating. It is using the method correctly. The goal is behavior change, not a perfect spreadsheet.

The long-term payoff of the snowball is not just the zero balance. It is the financial discipline you build by sticking with a plan for months or years. That discipline transfers to every financial decision you make afterward.

— Javier

Free tools at Apexapro to support your debt payoff plan

Tracking your progress with the right tools makes a measurable difference in how long you stay committed to a payoff plan.

Apexapro offers a free, browser-based collection of financial calculators that require no sign-up and no download. You can model your debt payoff timeline, calculate how extra payments reduce your total interest, and compare different repayment scenarios side by side. Every tool runs instantly in your browser and works in both English and Spanish. Whether you are building your first snowball plan or stress-testing a hybrid snowball-avalanche approach, the free financial tools at Apexapro give you the numbers you need to make confident decisions. New calculators are added regularly based on real user demand, so the catalog grows as your financial questions do.

FAQ

What is the debt snowball method?

The debt snowball method is a 6-step repayment strategy where you pay off debts from smallest to largest balance, rolling each freed-up payment into the next debt. It prioritizes psychological momentum over interest rate efficiency.

Which is better, snowball or avalanche?

The best method is the one you will complete. The efficiency gap between the two is often small when interest rates are similar, making the snowball's motivational benefits the deciding factor for most people.

Does the debt snowball method save money on interest?

Yes. Even without adding extra payments, the snowball method saves years and thousands in interest compared to paying only minimums on every account.

Can I customize the payoff order in the snowball method?

You can adjust the order to address emotional stress. Prioritizing a high-stress debt over a slightly smaller one improves engagement and long-term adherence without undermining the method's core logic.

How do I make sure extra payments actually reduce my balance?

Contact your lender directly and request that all extra payments be applied to your principal immediately. Some lenders default to crediting extra funds as future scheduled payments, which slows your payoff timeline.